Fertility Tech’s Next Chapter: Platforms, Not Point Solutions

By:

Angela Rastegar, Cofounder & CEO, Sunfish Technologies

Jessica Karr, Founder & Managing Partner, Coyote Ventures

Key takeaways from this article:

- The future of fertility innovation is shifting away from standalone tools and toward integrated platforms like Sunfish that combine financial planning, patient support, and care coordination into one connected experience instead of solving only a single problem in isolation.

- Fertility care is inherently complex, fragmented, and long-term, which creates friction for both patients and clinics. Patients often navigate months of treatment, multiple providers, administrative burdens, and significant financial uncertainty.

- In terms of venture capital, the majority of total capital flowed toward larger companies building scalable platforms that improve workflows, reimbursement, and patient access.

- The strongest fertility platforms will balance operational efficiency with human-centered support. Companies are not going to replace clinics, but work alongside them to simpify logistics.

Fertility treatments and assisted reproductive technology (ART) first emerged in the late 1970s. Since then, the industry has evolved in distinct waves; reshaping how care is delivered, accessed, and scaled.

What began in academic research settings in the 1980s became, by the 1990s, a fragmented ecosystem of physician-owned, capital-intensive local clinics that operated largely outside the venture capital market. For decades, fertility care and its supporting services remained mostly traditional, brick-and-mortar businesses.

Then came the inflection point. Around 2015, private equity consolidation accelerated, egg freezing entered the mainstream, and employer-sponsored fertility benefits expanded rapidly. Together, these forces transformed fertility into the venture-backed ecosystem we see today.

Since 2020, nearly $2 billion in venture capital has flowed into fertility and ART startups. And the market itself is growing quickly: by several estimates, the global fertility market is projected to grow from roughly $40 billion in 2025 to over $85 billion by 2034.

In this article, investor Jessica Karr of Coyote Ventures and CEO Angela Rastegar of Sunfish teamed up to analyze recent venture capital deals, and share what it signals about where the market is headed. Their analysis reveals that venture capital in fertility is not distributed evenly. In fact, the data shows a bimodal, “barbell” shape – capital clusters at the seed stage and again around later-stage breakouts, with a hollow middle in between.

That shape reveals where fertility innovation is accelerating, and why the next generation of category-defining companies will be embedded, interoperable platforms, not standalone point solutions. A “platform” doesn’t replace a clinic’s core systems; it embeds into existing workflows, integrates multiple capabilities, and reduces operational lift. The winners will share a common trait: flexibility; meeting clinics where they are while strengthening patient support and simplifying clinic workflows.

The Shape of the Money

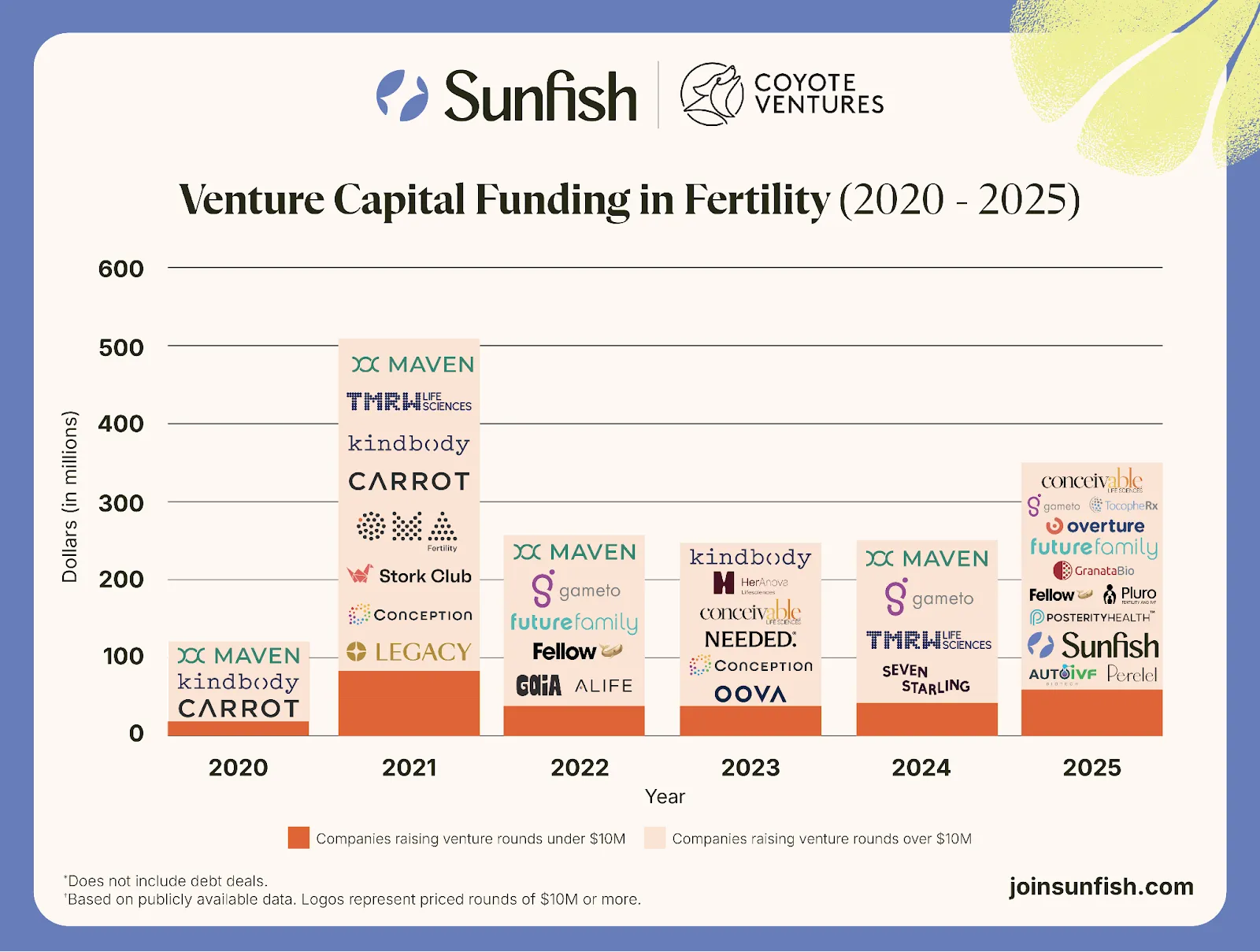

To map the market, we analyzed 160 publicly available fertility tech venture deals from 2020 to 2025, representing $1.8B in publicly reported equity financing from U.S.-headquartered companies.

Across the dataset, the majority of deals were small: 74% of the rounds raised were under $10 million. There appears to be an appetite for investors to support innovation at early stages. In many cases, these startups are set up to create point-solutions for lab automation, embryo storage, data interoperability, patient engagement, or financial access businesses.

On the other hand, about one quarter of the rounds went to a handful of companies that raised over $10 million - and represented 84% of the total capital raised. More specifically, these larger investments that improve infrastructure connect workflows, data, and patient access / reimbursement in ways that make clinics more efficient.

The result is today’s barbell market: a high-growth, fragmented ecosystem where "wedge" startups can secure seed funding with relative ease. While this fosters innovation, it also creates a "fragmentation tax" for clinicians, who are now inundated by a flood of point solutions that solve single problems but struggle to integrate into the broader practice.

We saw large rounds drive the market forward in 2021, and again, with a rebound in 2025.

Source: Sunfish Technologies and Coyote Ventures. Total equity funding by year based on publicly available data. Logos represent priced rounds of $10M+.

The implication is straightforward: it’s not enough to build a point solution. The companies that earn the biggest checks are building platforms that can provide multiple integrated solutions.

The Rise of Embedded, Interoperable Platforms

One of the reasons why infrastructure/platform solutions are so important is because fertility care is not a one-time transaction. Often, patients undergo a months-long journey that’s logistically complex, emotionally draining, and costly for patients. Internal data from Sunfish suggests that most people need approximately 3 rounds of IVF to be successful, representing dozens – often 40-60 – clinical encounters for the average patient.

Because of the operational complexity, the winners in fertility aren’t the companies with the slickest patient app—they’re the ones that make clinics easier to run where patients feel the most supported.

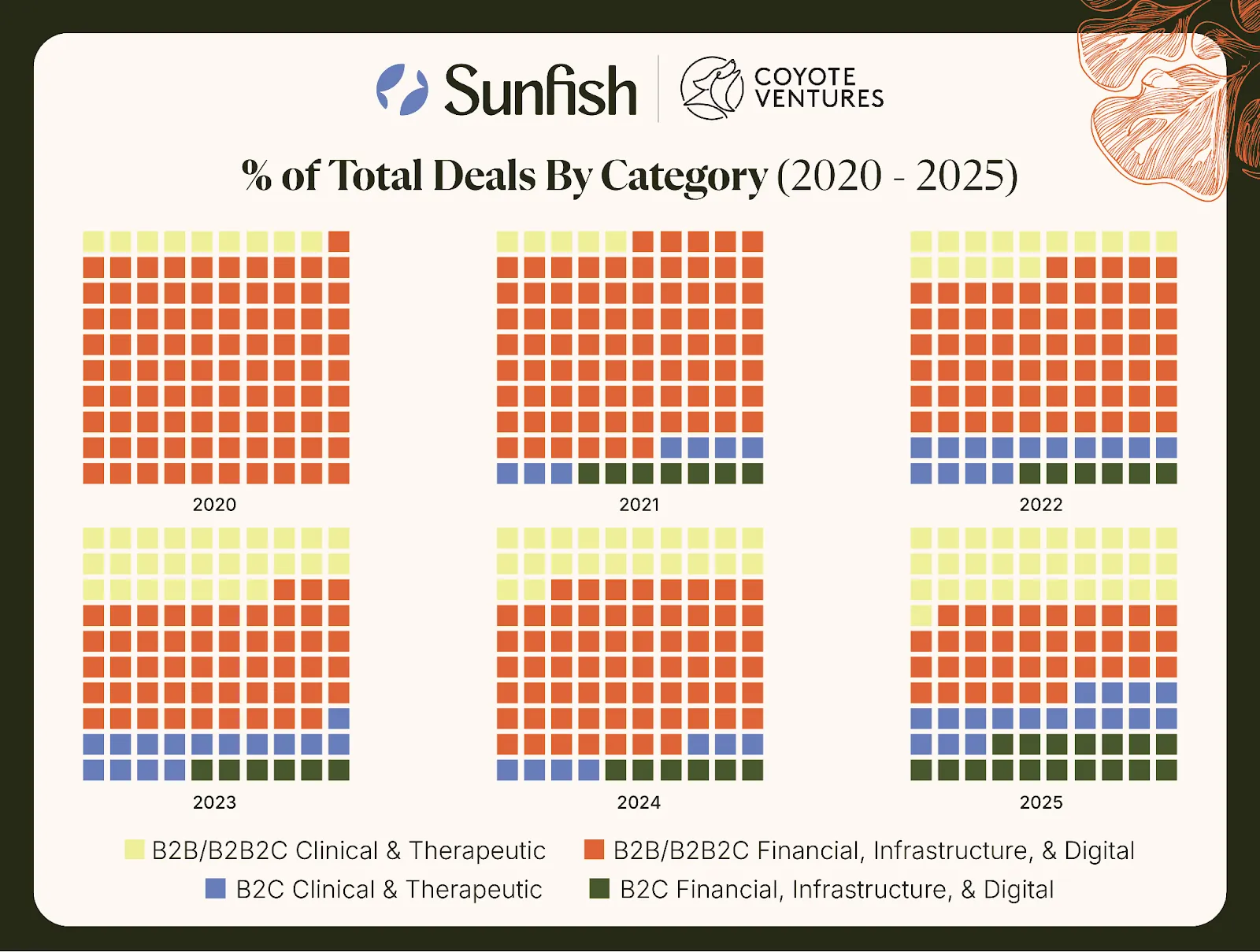

Across 2020–2025, as a portion of total funding, we saw most growth was driven by B2B and B2B2C companies: those building solutions for clinics and labs, as well as their patients. We divided these deals into Clinical and Therapeutic solutions (diagnostic tools, drugs, scientific innovation; think Conception, Gameto) and Financial, Infrastructure, or Digital tools (solutions for patient access, clinic workflows, lab tech, and patient care coordination; think TMRW, Conceivable, Sunfish, Maven).

In more recent years, B2C rounds are increasing among companies focused primarily on the end patient experience – especially in clinical and therapeutic categories. Think Fellow, Posterity, Needed, and the numerous apps and point solutions for fertility patients. (Caveat: some of these are seeking distribution through clinics in a B2B2C model now. If some of these players can deliver on a high quality consumer experience with B2B infrastructure, we’ll likely see other breakaway companies.)

Source: Sunfish Technologies and Coyote Ventures. Categories were assigned based on the primary product offered by each startup, and indicate the percentage of dollars in each category. We’re seeing more B2C innovation, alongside a steady foundation of B2B infrastructure.

Unlocking Growth: Holistic Solutions to Solve Capacity

The defining constraint in reproductive care today is not demand, but capacity. While the industry faces a massive "throughput" problem, patients are struggling with an "access" problem as the cost of IVF in the U.S. relative to GDP is significantly higher than in other developed nations. Consequently, the utilization of assisted reproduction remains low; only about 2% of babies in the U.S. are born via IVF today. This stands in stark contrast to the underlying need where the CDC reports that 1 in 5 couples struggle with infertility.

Rather than expecting clinics to navigate a proliferation of point solutions, winning software will embed into existing clinic environments and combine solutions through interoperability, creating a unified experience without additional operational burden. The emerging generation of winners are looking like end-to-end platforms that connect the full journey.

For example, cofounder and CEO Angela Rastegar explains: “As Sunfish has evolved, we’ve learned that improving outcomes requires supporting both the patient and the clinic across the full family building journey. We started as a patient financial solution, but we’ve evolved into a holistic solution. We help patients with guidance, financial readiness, and wraparound support through pregnancy, until they go home with a baby.”

“Most importantly, the way we support clinics is flexible to meet them where they are at: we can integrate into their workflows or stand alone, to reduce time-to-treatment, improve care coordination, and simplify financial and administrative handoffs,” continues Rastegar. Sunfish isn’t a lender; loans are one of the many components embedded within the solution, alongside care coordination and clinic workflow support.

Looking ahead, the next generation of winners will look less like single-purpose tools and more like end-to-end platforms that connect the journey:

- Improved Patient Support: Patient readiness; patient education; ongoing care coordination; financial support.

- Simplified clinical workflows: interoperable financial workflows, care coordination, and seamless integration with EMRs, labs, and existing clinic systems driven by data and AI innovation.

This shift is already visible in how the most durable companies are expanding: not by staying narrow, but by connecting more of the ecosystem.

Maria Molland, a growth stage healthcare investor at Frazier Healthcare Partners, explains: “From a late-stage investor perspective, fertility remains highly attractive, but the value creation is increasingly concentrated in infrastructure and services that sit adjacent to care delivery. The most compelling opportunities are in tech-enabled services that partner deeply with scaled clinic platforms — spanning lab and embryology technology, cryo and storage, revenue cycle management, payments, and data and analytics — all of which directly drive capacity, cost efficiency, and outcomes. By integrating with clinic workflows and data systems, these organizations can help standardize care delivery, improve cycle efficiency, and, critically, prove ROI for employers.”

The market is increasingly rewarding companies that build for continuity, designing systems that serve practitioners and patients in tandem.

2026 Predictions and Beyond

We expect a small number of scaled platforms will continue to raise large rounds. At the same time, early-stage innovation will remain active, because fertility continues to have many unsolved problems.

Value-Based Care

Thought leaders like David Sable have long pushed for a shift to helping patients have babies, not IVF Cycles. As coverage through employers and insurance expands, a focus on outcomes is even more important.

Sunfish offers money-back guarantee protection packages, and has already seen success: 70.8% of transfers among its patients have resulted in a successful pregnancy and graduation to OB-GYN, compared to a 54.3% national average reported by SART.

AI shifting to actually transforming care

“AI” tends to be overused by startups; implementing AI is helping to improve workflows, notetaking, etc., but we’re waiting to see transformational care. Winning solutions will need to be flexible to meet clinics where they are, in terms of the level of integration and automation desired.

We spoke with Maven Clinic’s CEO, Kate Ryder, who stated: “The next chapter of investment… will use data and AI to make fertility care more personalized, more efficient, and fully integrated into the broader healthcare system as essential care for families everywhere.”

Data as a moat

As fertility moves toward platform solutions, we believe that data increasingly becomes the defining advantage. Currently, the market still runs on fragmented systems and manual handoffs, which makes it difficult for clinics to track the full patient journey, measure outcomes consistently, and identify where cycles slow down or drop off.

The companies that break out in the next chapter will be the ones that can connect clinical data, lab data, patient-reported data, wearables, and financial workflows into a single operational view of care. That connectivity is what enables real interoperability, stronger analytics, and more personalized patient support over time. At Sunfish, we believe this also creates the foundation for AI to be genuinely useful—not just a layer on top of existing processes, but a tool that improves decision-making, cycle efficiency, and the reliability of care delivery.

Moving beyond fertility to longitudinal family building care

While the immediate hurdle is capacity, we believe the long-term opportunity lies in data integration. "The real upside is using longitudinal clinical and utilization data to expand upstream into pre-IVF risk identification and downstream into maternity and postpartum care," explains Molland of Frazier Healthcare Partners. By moving beyond isolated procedures, the industry can create "a more predictive, outcomes-driven fertility ecosystem that benefits patients, providers, and employers alike."

Summary

The companies that succeed will be the flexible ones—meeting each clinic where it is, supporting different levels of integration, and strengthening patient support while simplifying day-to-day clinic workflows. The companies that scale will be the ones that prove real value within the existing care ecosystem, delivering measurable ROI, improving patient outcomes, and integrating seamlessly into clinical workflows. “In a complex, clinic-driven market, lasting impact comes from solutions that work for providers as well as the patients they serve across the full family building journey,” says Jessica Karr, Founder and Managing Partner at Coyote Ventures.

What are you seeing? Which early-stage innovations are being overlooked? Which bets do you think will shape fertility’s next chapter?

Analysis based on publicly reported equity deals from U.S.-headquartered companies totaling $1.8B between 2020–2025. Does not include debt deals. A handful of B2B solutions captured the majority of fertility venture funding: Maven ($370M), Kindbody and KBI Services ($320+M), TMRW Life Sciences ($250M+), and Carrot Fertility ($60M+). It’s worth noting that Progyny, an employer benefit platform founded in 2008, went public in 2019 and thus wasn’t included in this analysis.